Business Update | August 30, 2017 | Author: Hdeel Abdelhady | Download PDF

On August 22, 2017, the Financial Crimes Enforcement Network (FinCEN) issued revised Geographic Targeting Orders (GTOs) designed to combat money laundering and related financial crimes in select U.S. residential real estate markets. The GTOs further expand the scope of GTOs issued in January 2016, expanded in July 2016, and renewed in February 2017. In tandem with the August GTOs, FinCEN issued an Advisory to Financial Institutions and Real Estate Firms and Professionals (the “Advisory”) and FAQs.

Money Laundering, and Illicit Finance Risks in Luxury Real Estate: Concerns and Rationale for GTOs

In the Advisory, FinCEN explains that luxury real estate markets are “vulnerable to penetration by foreign and domestic criminal organizations and corrupt actors, especially those misusing otherwise legitimate limited liability companies or other legal entities to shield their identities.”[i] FinCEN is not alone in its concern about beneficial ownership opacity generally and in the context of real estate transactions.

Concerns among U.S. and other G-20 officials and agencies about the use of shell companies to conceal money laundering and related crimes (e.g., corruption, sanctions and tax evasion, narcotics trafficking) have yielded policy and regulatory actions in recent years.[ii] Outside of the United States, proposals have been offered and action has been taken to identify beneficial owners in banking and other transactions. In the United States, steps have been proposed and taken to deprive individual actors of the evasive benefits of corporate opacity. For example, beginning in May 2018, U.S. banks and other “covered financial institutions” will be required to collect, record, and retain beneficial ownership information.[iii]

Real estate, particularly luxury real estate, has not been spared from policy and regulatory scrutiny.[iv] In the United Kingdom, a proposal for a register of foreign legal owners of property and their beneficial owners is advancing.[v] In the United States, FinCEN has not only issued and expanded GTOs, but also has cross-checked (with Bank Secrecy Act (BSA) data) and analyzed GTO-mandated information to gain “greater insight into illicit finance risks in the high-end real estate market.”[vi] Indeed, according to FinCEN, as of May 2, 2017, “over 30 percent of the real estate transactions reported under the GTOs involved a beneficial owner or purchaser representative that had been the subject of unelated Suspicious Activity Reports filed by U.S. financial institutions.”[vii]

As it appears that data collected through GTOs has thus far justified their expansion, it would not be unreasonable to expect additional expansions of FinCEN GTOs (nor would it be entirely surprising for FinCEN to treat, as a regularized or regulatory matter, real estate industry participants functionally as “financial institutions” (to an extent).[viii]

U.S. regulators are not alone in their concerns about the interplay between luxury real estate, money laundering, and other illicit activity. Congress members have also raised concerns. At an April 2017 BSA hearing of the House Financial Services Committee’s Subcommittee on Terrorism and Illicit Finance, one high ranking subcommittee member suggested that “GTOs be extended geographically and temporally, to apply nationwide and permanently.”[ix] Another subcommittee member expressed concerns that requiring reporting only by title insurance companies was insufficient, given the reduced incentive to obtain title insurance in all cash real estate transactions.[x] Others raised questions as to whether FinCEN’s GTOs (as of April 27, 2017) were sufficiently broad in other respects.[xi]

Given the high level and widespread nature of scrutiny of illicit activity in luxury real estate markets, it seems reasonable to expect FinCEN to, at minimum, continue to employ and expand GTOs in the foreseeable future. The remainder of this Business Update discusses core mechanics of the August GTO.

GTOs Applicability and Reporting and Records Retention Provisions

- Applicability. The GTO requires Title Insurance Companies and their subsidiaries and agents (together “TICs”) to collect, report, and retain beneficial ownership and additional information in connection with transactions for the purchase of residential real property in designated locales where such purchases are: (1) made by legal entities (e., non-natural persons), (2) without a bank loan or other “similar” external financing, and (3) funded, “at least in part,” with currency, check(s), money order(s), or funds transfer(s). Under the GTO, a TIC is a “Covered Business” and a transaction that meets the foregoing criteria is a “Covered Transaction.”

- Reporting and Records Retention. The GTOs impose reporting and records retention obligations on TICs, specifically the: (1) e-filing within 30 days of a Covered Transaction of a FinCEN Form 8300 through the Bank Secrecy Act E-filing system and (2) retention of “all records relating to compliance” with the GTOs for five years from the last effective date of the GTO (including renewal periods).

- FinCEN Form 8300 Information Gathering and Reporting. An e-filed FinCen Form 8300 must include the following information.

- Purchaser’s Primary Representative. The purchaser’s primary representative (g., an agent) must be identified and reported. Additionally, documentation verifying the representative’s identity must be collected and recorded—such documentation includes a driver’s license, passport, or “other similar identifying information.”[xii]

- Legal Entity Purchaser. The name, DBA (doing business as name), address, taxpayer or employer identification number, and additional information about the legal entity purchaser is required.

- Beneficial Owner(s) of Legal Entity Purchaser. The Form 8300 must include information about the Beneficial Owner(s) of the legal entity purchaser. The GTO defines a Beneficial Owner as “each individual who, directly or indirectly, owns 25% or more of the equity interests of the [legal entity] Purchaser.”[xiii]

Because indirect ownership is included, in cases where the legal entity owner is owned by one or more legal entities (directly or indirectly), a Covered Person will be required to search up the chain of ownership until natural persons meeting Beneficial Owner criteria are found. Where ownership structures are multi-layered or otherwise complex, the search for Beneficial Owners can be costly, administratively burdensome and, in some cases, raise red flags that might require further due diligence or weighing of potential risk.

As in the case of information required to verify the Purchaser’s Representative, a Covered Business must obtain and record a copy of the driver’s license, passport, or “other similar identifying documentation” or the Beneficial Owner(s). Such documents, along with others, should be considered part of “all records relating to compliance with” the GTO for the purposes of compliance with its records retention provisions.[xiv]

- Covered Transaction Information. In addition to the above, information about the Covered Transaction is required, specifically the: (1) closing date, (2) total funds transferred in any form, (3) total “purchase price,” and (4) address of the real property “involved in the Covered Transaction.”[xv]

- Unique Identifier and Covered Business Entity and Beneficial Ownership Information. The Covered Business is required to include in the Form 8300 the unique identifier “REGTO,” along with its basic information (g., name, address, nature of business, Employer Identification Number). If the Covered Business is an LLC, the following information is also required: the (1) name, address, and taxpayer identification numbers of “all of its members.”[xvi]

Covered Transactions: Addition of Funds Transfers and Hawaii Residential Real Estate Transactions

Covered Transactions—i.e., those subject to the information gathering, reporting, and records retention requirements of the GTO—are all cash residential real estate purchases, for specific minimum amounts and in specific locales, by legal entities such as limited liability companies, partnerships, corporations, and other business entities formed under the laws of a U.S. or non-U.S. jurisdiction.

- Funds Transfers Included. Notably, the August GTO expands the definition of “cash” to include “fund[s] transfers,” such as wire transfers. This is significant as is likely to capture substantially more transactions. Moreover, the inclusion of funds transfers is new to the Form 8300 reporting scheme. Thus, FinCEN’s clarification that the GTO should be followed where it conflicts with Form 8300’s instructions is relevant with respect to funds transfers.[xvii]

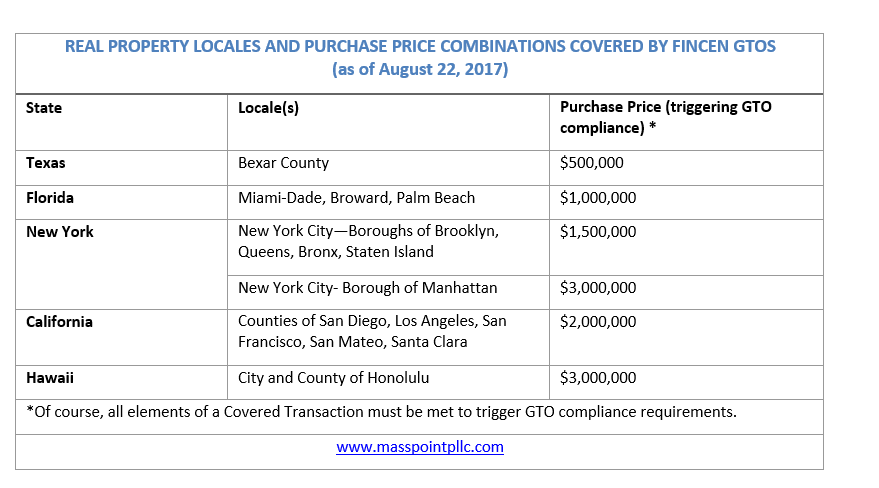

- Addition of City and County of Honolulu. The August GTO covers additional locales—the City and County of Honolulu, Hawaii—bringing targeted geographic and purchase price combinations to the following six.

Effective Date and Duration; Records Retention and Availability to FinCEN, Law Enforcement

The August GTOs take effect on September 22, 2017 and end on March 20, 2018 (the “Order Period”). For records retention purposes, the implications of the Order Period (which may be extended by future GTO renewals and/or expansions) are that “all records relating to compliance” must be retained for five years from March 20, 2018 (the last day of the GTOs) or a subsequent GTO end date if renewed or extended. The GTO also requires TICs to make such records “available to FinCEN or any other appropriate law enforcement or regulatory agency, upon request.”[xviii]

TICs should ensure that records are compiled and retained in a manner that meets the qualitative and accessibility objectives of the GTO, including that such records be stored in a manner that is “accessible within a reasonable period of time.”[xix]

Civil and Criminal Liability for Noncompliance

Pursuant to the GTO, a Covered Business and “any of its officers, directors, employees, and agents may be liable, without limitation, for civil and criminal penalties for violating any of the terms of this Order.”

Related MassPoint Publications

- U.S. Senators Raise National Security Concerns About Foreign Investment in U.S. Real Estate, May 2017.

- Congressional Hearing on Terrorism Financing Focused on Bank Secrecy Act Data Collection and Sharing and Effectiveness, April 2017.

- Proposals to Curb Foreign Investment in the United States Gaining Steam After the U.S. Election, November 2016.

- Proposed U.S. Rule Requires Banks to Collect Beneficial Ownership Information, November 2014.

NOTES

[ii] See, e.g., Jamie Smyth and George Parker, G-20 leaders back drive to unmask shell companies, Financial Times, Nov. 16, 2014.

[iii] Customer Due Diligence Requirements for Financial Institutions; Final Rule, 81 Fed. Reg. 29,398 (May 11, 2016) (to be codified at 31 C.F.R. 1010, 1020, 1023, 1024, and 1026) (the “CDD Rule”). See also, Hdeel Abdelhady, Proposed U.S. Rule Requires Banks to Collect Beneficial Ownership Information, Butterworths Journal of International Banking and Financial Law, November 2014 (discussing elements of the proposed CDD rule that are consistent with the final rule).

[iv] Commercial real estate has also garnered scrutiny, but not formally (yet) in the United States.

[v] See, e.g., Ali Qassim, U.K. Register of Overseas Beneficial Owners Raises Concerns, Bloomberg BNA, April 18, 2017.

[vi] Advisory at 2. The 30% figure was presented in FinCEN testimony before Congress in April 2017. See, e.g., MassPoint PLLC, Congressional Hearing on Terrorism Finance Probes Bank Secrecy Act Data Effectiveness, Lack of Beneficial Ownership Transparency, and Potential BSA and Patriot Act Amendments, infra note 9.

[vii] Id. at 5.

[viii] FinCEN has more than once noted that “persons involved in real estate closings and settlements” are “financial institutions” under relevant law, but have not been regulated as such by FinCEN. This and other statements could merely be descriptive of FinCEN’s authority vis-à-vis the real estate industry, or such statements may telegraph FinCEN’s policy or regulatory thinking. Time will tell. See, e.g., Advisory at 1.

[ix] MassPoint PLLC, Congressional Hearing on Terrorism Finance Probes Bank Secrecy Act Data Effectiveness, Lack of Beneficial Ownership Transparency, and Potential BSA and Patriot Act Amendments at 4, April 28, 2017.

[x] Id. at 4. It is worth noting here that title insurance companies often provide real estate settlement services even when no lender’s or owner’s title insurance policy is purchased. Thus, a title insurance company may be involved in an all cash transaction that does not involve the issuance of a title insurance policy. That said, it is accurate (and obvious) that FinCEN’s GTOs are not comprehensive as to, inter alia, transactions and geography. However, there are many ways that the purpose and letter of GTOs can be thwarted—for example, an individual can effectively have the power to obtain beneficial ownership of an entity after a real estate purchase is completed (and reported to FinCEN), such as by holding convertible debt that, at the time of a reportable real estate transaction, has not been converted into equity.

[xi] Id. at 4-5.

[xii] GTO at II.B.2.1.

[xiii] Id. at II.B.2.ii and III.A.1.i.

[xiv] Id. at III.C.

[xv] Id. at II.B.2.iv.

[xvi] Id. at II.B.2.v-vi

[xvii] Id. at II.B.1 (“Each FinCEN form filed pursuant to this Order must be: (i) completed in accordance with the terms of this Order and the FinCEN form 8300 instructions (when such terms conflict, the terms of this order apply).” (emphasis added).

[xviii] Id. at III.C.

[xix] Id.